Why Comprehensive Health Insurance Is Essential for Senior Citizens?

A friend of mine recently shared something that stayed with me. Her parents had always been healthy, so buying health insurance never felt urgent. Then her father needed to be admitted to the hospital for a few days. Thankfully, he recovered, but the hospital bill came as a bigger shock than the illness itself. That’s when she realized she should have looked into comprehensive health insurance for senior citizens much earlier.

This is something many families go through. We often think we’ll buy a policy “next month” or “after retirement,” until an unexpected medical emergency changes everything. A good health insurance plan can’t stop the health problems, but it can help you deal with them without any stress. In this blog, we’ll look at why comprehensive medical insurance for senior citizens matters, what it covers, how to choose the right plan, and the things you should know before buying one in 2026.

“Since 1 April 2024, IRDAI’s Master Circular on the Health Insurance business has removed the maximum entry age. In today’s world, insurers have the option to and do accept clients at age 70, 75, 80, or without any maximum age limit, depending on the insurance product being offered.”

Table of Contents

What is Comprehensive Health Insurance for Senior Citizens?

Comprehensive health insurance for senior citizens is a specially tailored insurance policy that provides extensive coverage for medical expenses incurred during their later years. These plans go beyond basic coverage and encompass a wide range of healthcare needs, including hospitalisation, pre and post-hospitalisation expenses, diagnostic tests, and even critical illness coverage.

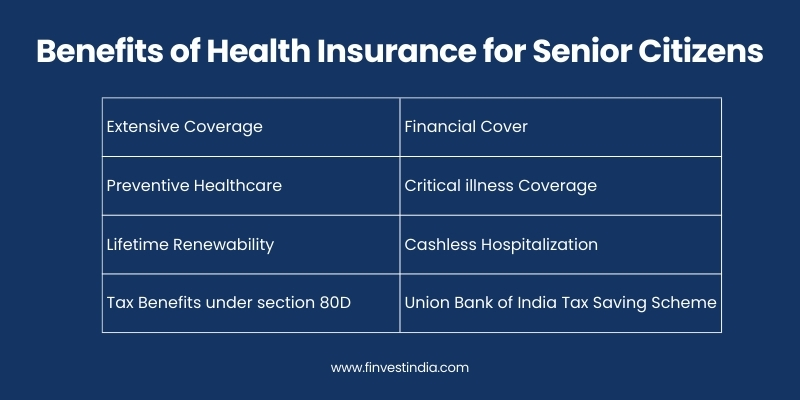

What are the Benefits of Comprehensive Health Insurance for Senior Citizens?

- Extensive Coverage: Unlike standard health insurance plans, comprehensive health insurance for seniors offers broader coverage, ensuring that a myriad of medical expenses is taken care of.

- Financial Cover: In uncertain times, health insurance policies ensure that you get protected from unexpected and expensive financial costs and have a safety net to fall back on. While different companies offer varying products, almost all policies cover a wide range of illnesses and their ailments.

- Preventive Healthcare: Many comprehensive plans include preventive healthcare services, encouraging seniors to undergo regular health check-ups, leading to early detection and prevention of potential health issues.

- Critical Illness Coverage: Senior citizens are often more susceptible to critical illnesses. Comprehensive health insurance plans typically include coverage for critical illnesses, offering financial protection during challenging times.

- Lifetime Renewability: A crucial feature of these plans is the option for lifetime renewability, allowing seniors to continue their coverage without the fear of losing it in their later years. Medical insurance for senior citizens can not only be taken at the maximum age of 65 years but can also be renewed up to 80 years of age. Some companies allow renewability up to the age of 90 years, provided there has been no break in payment of premium since the policy was first taken.

- Cashless Hospitalization – Most companies that offer insurance plans to senior citizens allow cashless transactions, i.e., a benefit where the hospital can claim payment for the rendered treatment directly from the insurer.

- Tax Benefits U/S 80D – It is important to note that health insurance for either yourself or for family members has the added benefit of reducing taxable income. If you purchase a health plan, you are eligible to get a tax deduction under Section 80D.

What's New in Senior Citizen Health Insurance (2026)

Several regulatory changes introduced by IRDAI between 2024 and 2026 have made senior citizen health insurance more accessible and consumer-friendly:

- No universal maximum entry age. Insurers can no longer refuse a policy to someone purely for being over 65. (IRDAI Master Circular, 29 May 2024)

- Premium hikes for seniors are now capped. Insurers need IRDAI’s prior approval to raise a senior citizen’s premium by more than 10% in a year.

- GST on individual and senior citizen premiums dropped from 18% to 0%.

- Pre-existing disease waiting periods are capped at 36 months industry-wide, down from up to 48 months.

- The moratorium period, after which insurers can’t deny a claim for non-disclosure (barring fraud), is now 5 years, down from 8.

- Cashless treatment is available at any hospital, not just network hospitals, under IRDAI’s “Cashless Everywhere” framework.

- The free-look period to review and cancel a new policy has been extended from 15 to 30 days.

- Dedicated grievance and claims channels for senior citizens are now mandatory for every insurer.

- Ayushman Bharat PM-JAY now offers every citizen aged 70+ up to ₹5 lakh a year in free coverage, regardless of income.

Why this matters?

A hospitalization that costs ₹5 lakh today could cost well over ₹8 lakh within five years if medical inflation continues at current levels. Industry data puts medical inflation at roughly 12-14% a year in 2025-26, against general CPI inflation of 3-4%. Senior citizens now spend a meaningfully higher share of their income on healthcare than they did a few years ago, and family floater premiums industry-wide have climbed sharply over the same period.

What a Comprehensive Senior Citizen Medical Insurance Policy Typically Covers?

- Hospitalisation expenses: room rent, doctor’s fees, surgery, and medication, subject to the sum insured.

- Pre- and post-hospitalisation: commonly 30-60 days before and 90-180 days after admission.

- Daycare procedures that don’t need a 24-hour stay, such as chemotherapy or dialysis.

- Organ donor expenses for transplant surgeries.

- Modern treatment methods: robotic surgery, oral chemotherapy, and similar procedures, in many newer plans.

Waiting Periods, Explained

This is one of the most misunderstood parts of any senior citizen policy:

| Type | What it covers | Current range |

|---|---|---|

| Initial waiting period | Any illness (not accidents) in the first 30 days | 30 days |

| Pre-existing disease (PED) waiting period | Conditions the applicant already had – diabetes, hypertension, etc. | 1-4 years, capped at 36 months by regulation |

| Specific disease/procedure waiting period | Named conditions like cataracts, hernia, joint replacement | 1-2 years, insurer-specific |

| Moratorium period | Point after which claims can’t be denied for non-disclosure, fraud excluded | 5 years |

Exclusions to Check Carefully

Beyond the general waiting-period exclusions above, most senior citizen policies also exclude:

- Cosmetic or plastic surgery, unless required after an accident.

- Experimental or unproven treatments not backed by established medical protocols.

- Self-inflicted injury.

- Treatment received without a valid prescription.

- Obesity/bariatric treatment, unless specifically added as a rider.

- Fertility treatment.

- Non-medical consumables (gloves, syringes, administrative items), often billed separately by hospitals and excluded from claims.

- Illness or injury arising from war or nuclear events.

“Getting health insurance is most helpful when it’s part of a larger plan for retirement, and not something you decide to get it at the last minute. As part of our process at Finvest India helping clients create their retirement plan. We help them make a full plan that includes their finances, their willingness to take risks, and their spending during their retirement. Health insurance is a key part of this plan. Spending as much time looking at a client’s co-payment policies, room-rent ceiling, and riders as looking at the sum covered is necessary because these things are usually more important in the claims process.”

Section 80D Tax Benefits (Current for FY 2025-26)

| Category | Maximum deduction |

|---|---|

| Self/spouse, below 60, plus dependent children | ₹25,000 |

| Self/spouse, senior citizen (60+) | ₹50,000 |

| Parents, below 60 | Additional ₹25,000 |

| Parents, senior citizens (60+) | Additional ₹50,000 |

| Preventive health check-up | Up to ₹5,000, within the above limits |

A senior citizen with senior citizen parents can claim up to ₹1,00,000 in total. Important: this deduction applies only under the old tax regime; it cannot be claimed under the new regime, which is worth checking before filing given how many taxpayers now default to it. Premiums must be paid via a non-cash mode to qualify. Income Tax Department

Compare Top Comprehensive Health Insurance Plans for Senior Citizens

| Plan Name | Entry Age | Sum Insured Options | Lifetime Renewability | Waiting Period for Pre-Existing Conditions* | Notable Feature |

|---|---|---|---|---|---|

| HDFC ERGO Optima Secure | 61 yrs onwards | ~ ₹2 lakh to ₹5 lakh | Yes | ~4 years | Doubled cover from Day 1 (“Secure Benefit”) |

| Care Senior Health Advantage | 60 yrs+ (no upper age in some variants) | Up to very high covers (crores in some) | Yes | From 2nd year on many illnesses | No co-payment in some variants; large sum insured options |

| Cholamandalam Flexi Health Supreme | Up to 75 years | ₹5 lakh to ₹5 crore+ | Yes | From 3rd/4th year depending on variant | Global hospital cover add-on; lifetime renewability to high age |

| Star Senior Citizens Red Carpet | 60-75 yrs | ~ ₹1 lakh to ₹25 lakh | Yes | From 2nd year | No pre-acceptance medical screening irrespective of age |

How to Buy Health Insurance: A Practical Step-by-Step

- Assess medical needs: existing conditions, family history, and the realistic cost of care in your city.

- Compare insurers: request quotes for the same sum insured and city from at least 3-4 insurers.

- Check the PED waiting period and whether a reduction rider is available if needed.

- Review the co-payment clause: a lower co-pay usually means a somewhat higher premium, but less out-of-pocket exposure during a claim.

- Compare network hospitals: confirm your preferred hospitals are cashless-enabled with that insurer.

- Read the exclusions in full: not just the brochure summary.

Buy online or seek help with health insurance services in Bangalore. You should use the 30-day free-look period to check the actual policy copy before you sign.

Comprehensive Health Insurance for Senior Citizens: Finvest India

Comprehensive health insurance helps senior citizens manage their medical expenses without putting too much strain on their savings. For most retirees, the biggest danger isn’t one hospital cost; it’s recurrent medical expenses over several years. It is more important to buy a policy that gives you appropriate coverage, shorter waiting periods, and good claim support than just go for the lowest cost. Therefore, Finvest India is an excellent option to get into practical insurance planning. The bottom line is to choose a plan that actually works for the person, not just the price.

Disclaimer: This article is for general informational purposes only and does not constitute financial, tax, insurance, or legal advice. Regulations, tax limits, GST rates, and insurer terms are subject to change; please verify current details directly with the IRDAI, the Income Tax Department, and your chosen insurer before making a purchase decision.