NRI Returning to India: A Practical Financial Checklist for a Smooth Transition

After years of building a life abroad, coming back home sounds simple until the money side shows up. An NRI returning to India often has to deal with a pile of small but important things at once, bank accounts that need to be changed, taxes that work differently now, investments that may not fit the new status, and documents that suddenly matter more than they did before. It usually starts with one innocent question, like “Can I keep using this account?” and then turns into a long list of checks. That is the part many people do not expect.

The good part? None of this has to be overwhelming. With a little planning and the right information, you can avoid costly mistakes and make the move much smoother. In this blog, we will go through the main financial steps you should handle before and after returning, so the move feels less messy and much easier to manage.

Table of Contents

Why Financial Support Matters for an NRI Returning to India?

When you relocate to India, you don’t just change your home, you change your finances.

Many NRIs moving back to India have problems with their taxes, bank accounts, pensions, investments made overseas, foreign transfers etc. These problems can lead to more problems in the future if they are not dealt with properly.

A detailed financial strategy keeps you on top of things and reduces the possibility that you’ll overlook critical changes or compliance dates.

Above all, it safeguards the money and investments you’ve worked so hard to put up.

Financial Steps to Take Before Leaving Your Current Country

One of the smartest things NRIs returning to India can do is start preparing before you relocate.

1. Begin with a review of your work-related benefits. See if you are eligible for any outstanding bonuses, stock options, retirement contributions or pension payments. You might find it harder to get these advantages once you have left the country.

2. It’s also a good idea that you get the important papers together:

- Tax returns (last 3–5 years).

- Bank statements.

- Investment records.

- Insurance documents.

- Pension account information.

- Property-related paperwork.

3. Don’t forget to review your overseas bank accounts as well. You may still need some if you plan to receive overseas income or pension payments in the future. Before you send a large sum of money to India, compare the currency rates and find out what paperwork is needed.

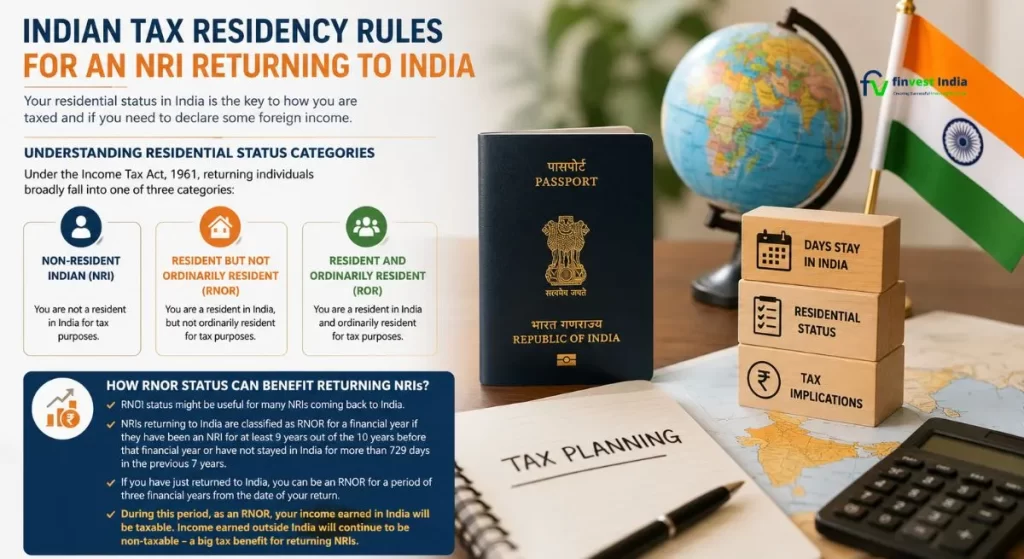

Indian Tax Residency Rules for an NRI Returning to India

Your residential status in India is the key to how you are taxed and if you need to declare some foreign income.

Understanding Residential Status Categories

The change of residential status under Indian tax laws depends mainly on the number of days you stay in India and other conditions prescribed under the tax laws.

Under the Income Tax Act, 1961, returning individuals broadly fall into one of three categories:

- Non-Resident Indian (NRI).

- Resident but Not Ordinarily Resident (RNOR).

- Resident and Ordinarily Resident (ROR).

How RNOR Status Can Benefit Returning NRIs?

RNOR status might be useful for many NRIs coming back to India.

NRIs returning to India are classified as RNOR for a financial year if they have been an NRI for at least 9 years out of the 10 years before that financial year or have not stayed in India for more than 729 days in the previous 7 years.

If you have just returned to India, you can be an RNOR for a period of three financial years from the date of your return. During this period, as an RNOR, your income earned in India will be taxable. Income earned outside India will continue to be non-taxable – a big tax benefit for returning NRIs.

2026 Update: On 13 February 2025, the Indian government approved the Income Tax Bill 2025. It came into effect on April 1, 2026. High income NRIs and PIOs who earn at least Rs 15 lakh from Indian sources will have to stay for 120 days instead of 60 days to be considered a resident.

Most NRIs returning to India are not aware of the significance of the RNOR window. At Finvest India, we advise our clients to plan their day count carefully before moving. This is because even a 15-20 day delay in when you return can imply the difference between one year and three years of RNOR security on your foreign income. You can adjust the way your global portfolio is arranged at this time before full resident taxation begins.

How an NRI Returning to India Should Review and Restructure Bank Accounts?

Your banking arrangements should be one of the first things you review after returning.

1. NRE vs Resident Account: What to Do With Your Bank Accounts When You Return to India?

NRE accounts are for the people living outside India. Generally, such accounts are required to be renamed when you become a resident under the applicable legislation.

Consequently, converting NRE / NRO accounts after becoming a resident is a key step that shouldn’t be missed.

If you don’t update your account status, you may have compliance concerns in the future.

You may also have to change your NRO accounts to show your new place of residence.

2. Should You Open a Resident Foreign Currency (RFC) Account?

If the RFC account holder is a returning resident, foreign funds can be retained in India if the conditions are met. As per the RBI’s rules on RFC accounts, this account can be funded from specified sources such foreign income, profits from assets located overseas and transfers from NRE/FCNR deposits that are already open.

This may be of use if you:

- Plan for pension payments from overseas.

- Getting overseas income all the time.

- Wish to keep savings in foreign currencies.

When you are examining your accounts, don’t forget to update nominee data, contact information and residency records with your bank.

Evaluate Your Investments Before Returning to India

Going home to India is an excellent time to review your financial portfolio again.

Many NRIs throughout the years have built up investments across many nations. They could be mutual funds, real estate, stocks, retirement accounts, fixed deposits etc.

Before you make any changes, understand the impact your return may have on taxation and reporting requirements.

1.Reviewing Mutual Fund, Insurance, and Bank Investments

Your financial goals may be much different than when you first moved abroad.

Perhaps building wealth was your priority when you lived abroad. When you return, goals tend to change towards retirement planning, buying a home, supporting family or earning a regular salary.

Look at your:

- Mutual funds.

- Fixed Deposits.

- Investments in insurance.

- Position in stock.

- Bank deposits.

2.Asset Allocation and Currency Risk

Many NRIs who have returned continue to own investments outside India.

Keeping some exposure to international markets may help you diversify your portfolio. Equally important is understanding the proportion of your wealth that is exposed to currency risk.

Usually, it’s better to shift everything gradually and in balance rather than all at once.

Understand Tax Implications on Global Income

Taxes are often one of the most confusing aspects of moving back to India.

The tax implications after returning to India depend largely on your residential status.

1. Tax Implications for NRIs Who Become Resident Indians — What Changes?

If you change your residential status from NRI to resident then the tax liabilities can be different.

Your taxability of income received outside India depends on your Residential Status.

For example:

- Interest on foreign bank accounts.

- Income from rental of foreign immovable property.

- Dividends on foreign investments.

- Foreign pension income (FPI)

2. Double Taxation Avoidance Agreements (DTAA)

India has income tax agreements with several nations of the world.

The deals are aimed to prevent the income from being taxed twice. Understanding how the DTAA laws apply to your individual situation can help you avoid excessive tax charges.

What If You Move Back to India? What Happens to Your 401(k)

If you are in the US and have a 401(k) retirement account, taxes are something you need to know about before you start withdrawing funds after moving back to India. Many returning NRIs feel that they can just transfer the money to India. But the money has to be liquidated first from a 401(k). In most cases, you may owe U.S. taxes and a 10% early withdrawal penalty if you make withdrawals before age 59½.

The withdrawn amount is normally credited to your US bank account first and then transferred to your NRE or NRO account in India. While some financial planners and returning NRIs want to delay the withdrawals for a few years to perhaps reduce the total tax burden, others prefer to keep the money invested till retirement. How you do it is decided by your residential status, tax position, retirement goals, and future plans in India.

Foreign Asset Disclosure Requirements

Many returning NRIs continue to own assets abroad, such as bank accounts, investments, pensions and property.

If you’re an Indian resident, you may be required to declare certain abroad assets when you file your tax return in India.

Manage Retirement and Pension Benefits

Your move is a good time to put some extra attention on retirement planning.

- If you have abroad pension accounts, check withdrawal rules, tax implications and transfer choices before you do anything.

- Different countries have different legislation and what works in one jurisdiction may not operate in the other.

- It is also an excellent opportunity to review your retirement goals depending on your lifestyle in India.

- You should consider things like medical costs, inflation and your long-term income demands when you’re planning for retirement.

Reassessing Insurance Coverage as an NRI Returning to India

Your insurance needs might change after you move.

- You may not be covered by foreign health insurance policy in India. So, consider local health insurance options first such as term life insurance from IRDAI-regulated insurers in India.

- Also evaluate your life insurance to be sure it covers your family’s financial needs.

- You might also want to look into critical illness coverage and other protection programs.

Plan Your Real Estate and Property Finances

Property-related decisions are high on the priority list for NRIs returning to India.

- If you already have property in India, check ownership papers, leasing agreements and property tax records.

- If you’re going to buy a house, spend some time looking at affordability and financing choices before you commit.

- It’s also vital to understand how rental income is taxed and whether any existing home loans need to be updated after you return.

Create a Financial Safety Net During Transition

Moving is more expensive than you know.

- Rental deposits, vehicle purchases, school admissions, furnishings and household setup expenditures may add up fast.

- An emergency fund can help you pay for those costs without messing with your long-term assets.

- Many financial advisers suggest keeping enough cash on hand to cover several months of living expenses.

Update Your Financial Records and Compliance Documents

Administrative tasks may not seem exciting, but they’re essential.

Updating KYC and FATCA Declarations

One of the first things you should do when you come back is update KYC and FATCA declarations.

- You are required to intimate banks, mutual fund houses, insurance providers and brokerage businesses about change in your residential status.

- You should also check and update:

- PAN details

- Aadhaar details

- Passport data

- Details of Nominee

- Contact information across financial institutions

Estate Planning and Wealth Transfer Considerations

Planning an estate is especially important where assets are located in a number of different countries.

- Review any existing wills to see if they reflect your current assets and family situation.

- If you have investments or property in more than one country, you should consider cross-border inheritance planning.

- When you move, make sure your powers of attorney and beneficiary designations are still valid.

Financial Mistakes to Avoid as an NRI Returning to India

Some of the most common mistakes that returning NRIs make are:

- Delaying residential status updates.

- Failing to respect the tax residency rules

- Forget to get NRE accounts converted.

- Ignoring the insurance needs.

- No investment review.

- No requirement to disclose foreign assets.

For example:While updating your residential status and reviewing your investments are essential, it’s equally important to understand the common investment mistakes NRIs should avoid before making financial decisions after returning to India.

Complete NRI Returning to India Financial Checklist

| Financial Area | Action Required | Key Deadline / Authority |

|---|---|---|

| Tax Residency | Determine whether you qualify as Resident and Ordinarily Resident (ROR), Resident but Not Ordinarily Resident (RNOR), or Non-Resident Indian (NRI) for tax purposes. | Before filing your first Indian Income Tax Return (ITR); Income Tax Act, 2025. |

| FEMA Compliance | Understand the change in your residential status under FEMA and its impact on banking, investments, and asset holdings. | Effective from the day you return to India; RBI FEMA Master Directions. |

| Investments | Review and reorganise your Indian and overseas investments to ensure compliance with tax and FEMA regulations. | Within a reasonable time after returning; RBI FAQs on NRI Accounts. |

| Insurance | Reassess your health, life, and other insurance coverage based on your new residency status. | Ideally during the RNOR period. |

| Retirement Planning | Evaluate overseas pensions, NPS, EPF, and other retirement savings for tax efficiency and portability. | At the time of transition; PFRDA guidelines. |

| Documentation | Update your PAN, Aadhaar, KYC records, residential status, and FATCA/CRS declarations across financial institutions. | As soon as possible after returning to India. |

| Estate Planning | Review and update wills, nominations, beneficiary details, and succession plans to reflect your new residency. | Within the first year of returning. |

| Foreign Asset Disclosure | Report foreign assets and overseas income in Schedule FA of your Indian ITR, if you become an ROR. | By 31 July of the relevant Assessment Year (unless the due date is extended); Income Tax Act. |

| KYC / FATCA | Update your KYC, FATCA, and CRS declarations with banks, mutual funds, brokers, and other financial institutions. | Promptly after returning to India. |

| Banking | Convert NRE/NRO accounts to resident accounts and consider opening a Resident Foreign Currency (RFC) account, if eligible. | Within a reasonable time after your return; RBI FAQs on NRI Accounts. |

When Should You Consult a Financial Expert?

You can handle most of the moving process you but it can be helpful to have some professional advice.

- Several foreign corporations provide income in multiple avenues.

- A lot of foreign investment.

- Tax residency is complex.

- Cross-border inheritance issues.

- Retirement planning needs to be comprehensive.

Finvest India works with returning NRIs as part of their financial planning, not only as compliance. Moving from NRI to resident is one of the most financially significant movements a person can make, and the first 12–18 months often determine their tax status and wealth trajectory for the next decade. Our team helps clients create a staged plan that includes residential status, portfolio restructuring, retirement readiness, and regulatory compliance.

What Every NRI Returning to India Should Do?

For an NRI returning to India, the move is more than just booking a flight and settling into a new home. Taxes, bank accounts, investments, insurance, financial record, all need attention. If you take care of these areas early, you’ll save yourself a lot of unnecessary worry and make smarter financial decisions down the road. At first, it may seem overwhelming but with a clear plan it may make a huge difference. Working at Finvest India, we often see how well-prepared NRIs can settle back into India with more confidence, clarity, and financial peace of mind.

If you need personalised guidance, Finvest India’s NRI Investment Services can help you navigate taxation, banking, investment restructuring, and cross-border financial planning with confidence.

Disclaimer: This blog is for educational purposes only and is based on June 2026 rules and regulations, including the April 2026 Income Tax Act 2025. Tax and FEMA rules change. For personalized advice, seek a Chartered Accountant and FEMA-registered expert.